“Do I really need to wait 6 months to refinance?”

I get this text message almost every week. Usually, it’s from a homeowner who just closed on a house, only to see interest rates drop a quarter-point the very next month. Or, it’s someone who needs cash for an emergency renovation and thinks they are stuck.

Here is the honest truth: No, you don’t always have to wait.

That “6-month rule” you hear about? It’s often a myth, or at least, a misunderstanding of how different loan types work. While learning the technical side of how to refinance a mortgage loan is helpful, what you really need is the specific timeline for your situation.

If you move too fast, you risk a hard inquiry on your credit for nothing. If you wait too long, that market dip might disappear.

Since every lender has different “overlays” (their own internal rules on top of federal guidelines), I always tell my clients to double-check their specific eligibility first.

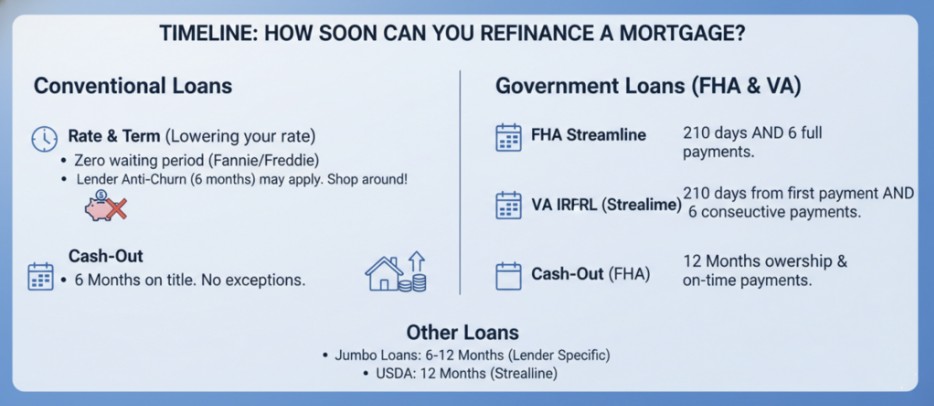

Timeline: How Soon Can You Refinance a Mortgage?

In the mortgage industry, we call the waiting period “Seasoning.” It’s basically the age of your loan. But here is where it gets tricky: the rules change completely depending on whether you have a Conventional, FHA, or VA loan.

Let me break down what I actually see in the field vs. what the generic guidelines say.

Conventional Loans (Fannie Mae & Freddie Mac)

- Rate & Term (Lowering your rate): Believe it or not, there is often zero waiting period from the agencies. If you closed yesterday and rates crashed today, Fannie Mae technically allows you to refinance tomorrow.

- The Insider Catch: Just because Fannie Mae allows it doesn’t mean your lender will. Most lenders get hit with an “Early Payoff Penalty” (EPO) if you refinance within 6 months. Because of this, many lenders will tell you their policy is 6 months, even if the actual guideline doesn’t require it. You might just need to find a new lender to do the deal.

- Cash-Out: This is stricter. You need to be on the title for at least 6 months before you can pull equity out. No exceptions here.

Government Loans (FHA & VA)

Uncle Sam is stricter to prevent “churning”, basically, stopping predatory lenders from refinancing veterans and FHA borrowers every month just to collect fees.

- FHA Streamline: You can’t just count months. You need to hit two specific targets: 210 days must have passed since your closing date. You must have made 6 full monthly payments.

- VA IRRRL (The VA Streamline): Similar to FHA. You need 210 days from your first payment date, and 6 consecutive payments. If you miss that by one day, the loan gets rejected.

- Cash-Out (FHA): You are looking at 12 months of ownership and on-time payments.

Jumbo & USDA

- Jumbo Loans: Since private banks hold these, they make their own rules. Expect a hard 6 to 12-month wait.

- USDA: Usually requires 12 months of seasoning for their streamline programs.

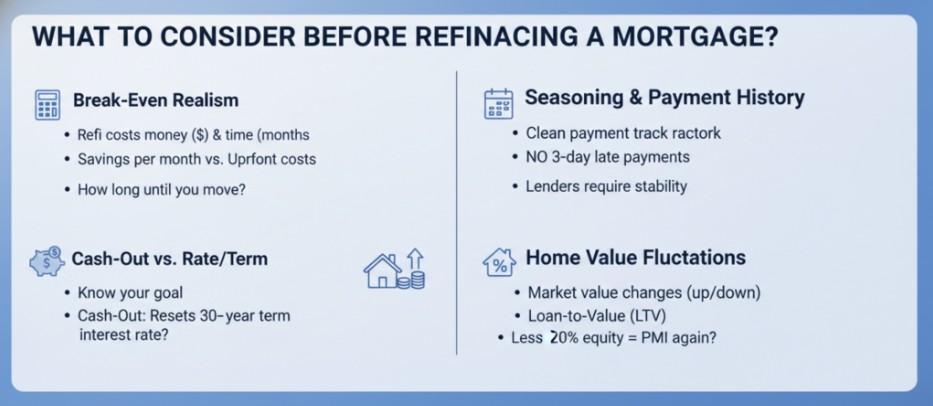

What to Consider Before Refinancing a Mortgage?

Just because a lender can refinance you next week doesn’t mean it’s a smart financial move. I’ve seen homeowners rush to save $40 a month, only to realize they paid $3,000 in closing costs to get it. That’s bad math.

Before you sign anything, look at these factors:

- The “Break-Even” Realism: Forget the interest rate for a second. Look at the costs. If the refinance costs $3,000 and saves you $150 a month, it takes 20 months just to break even. If you plan to sell the house in a year, you are actually losing money by refinancing.

- Seasoning & Payment History: This is the deal-breaker. Have you paid your mortgage on time every single month? One 30-day late payment in the last 6 months will kill your application instantly. Lenders want to see a clean track record.

- Cash-Out vs. Rate/Term: Know your goal. Taking cash out resets your amortization schedule (you start over at 30 years) and usually comes with a slightly higher rate. Is the immediate cash worth the long-term cost?

- Home Value Fluctuations: If you bought at the peak of the market and values have dipped, your Loan-to-Value (LTV) might be too high. If you don’t have 20% equity, you might get stuck paying Mortgage Insurance (PMI) again, which eats up your savings.

Frequently Asked Questions

Q1. How long do you have to wait before you can refinance a mortgage?

Answer: It depends on the loan. For a standard Conventional loan (no cash out), you can often refinance immediately, though many lenders prefer a 6-month wait. For FHA and VA loans, it’s a strict 210-day wait plus 6 monthly payments. For cash-out, expect to wait 6 to 12 months.

Q2. How long does it take to refinance a house with cash-out?

Answer: Don’t confuse the “waiting period” with the “processing time.” First, you usually need to own the home for 6 months (Conventional) or 12 months (FHA) to be eligible. Once you apply, the actual paperwork, appraisal, and underwriting typically take 30 to 45 days to close and get your money.

Q3. How quickly can I refinance after buying a home?

Answer: If you have a Conventional loan, you might be able to refinance as soon as you make your first payment, assuming you can find a lender willing to do it (watch out for those who have Early Payoff penalties). If you have an FHA or VA loan, you are locked in for roughly 7 months minimum.

Q4. What is the 6-month refinance rule?

Answer: This usually refers to Title Seasoning. It’s a safeguard that requires you to appear on the property title for at least 6 months. It prevents people from buying a house and immediately treating it like an ATM. For cash-out deals, this 6-month clock is mandatory.

Conclusion

Refinancing isn’t just about grabbing the lowest headline rate. It’s about timing.

The window to refinance opens at different times for everyone, from 0 days for some conventional borrowers to 12 months for FHA cash-out applicants. The rules are rigid, but the opportunities are real if you strike at the right moment.

Navigating the “210-day rule” or calculating your break-even point can be a headache. You don’t want to rely on guesswork when thousands of dollars are on the line.

My advice? Get a professional pair of eyes on your mortgage.

Check out Bluerate. We use smart tech to match you with local experts who can look at your specific loan date and tell you, “Yes, you can refinance now,” or “Wait two more months.” It’s free, it’s easy, and it ensures you make the move when it actually makes sense for your wallet.